{kind=link}

NEW DELHI: Multiple courts have now ruled that online games are a ‘game of skill’, as opposed to gambling which is a ‘game of chance’.

Prime Minister Narendra Modi’s interaction with Indian gamers, including Animesh Agarwal and Mithilesh Patan earlier this month, was more than just about sports and attracting young voters ahead of the Lok Sabha elections. The meeting underscored the growing significance of the gaming industry and the government’s interest in its development. The online gaming segment has emerged as a powerhouse of innovation, engagement and economic potential, with recent years witnessing a captivating surge in online gaming’s popularity, propelled by factors such as widespread smartphone penetration, enhanced internet connectivity, burgeoning youth population, heightened awareness and the development of local gaming content tailored to individual preferences.

Raghav Anand Partner, Ernst & Young Parthenon, points out that the online gaming segment has historically attracted substantial investor interest with investments worth Rs 22,931 crore from both domestic and global sources between FY20 and FY24 year-to-date. India continues to be a “mobile first” market, with 94% of its total gamer base engaging in mobile gaming experiences, with the online mobile gaming emerging as a US$1.5 billion sunrise sector, with 38% CAGR which will take the value to US$5 billion by 2025, according to an Ernst & Young report.

According to the All India Gaming Federation, India’s gaming industry attracted US$575 million between 2014 and 2020. However, in 2021 and Q1 of 2022 alone, US$1.7 billion was invested in the Indian online skill gaming sector. Currently, there are three online skill gaming companies which have achieved the status of unicorns. Current industry estimates that over 100,000 direct jobs have been created thus far, with the expectation that over 500,000 direct and indirect jobs would be created by the sector by 2028.

However, after an adrenalin charged compounded annual growth rate (CAGR) of 28% over the last 3 years to reach Rs 16,428 crore in FY23, India’s overall online gaming segment is looking for expeditious solutions to a slew of challenges, ranging from unclear regulatory environment, stalemate over the process of setting up self-regulatory bodies (SRBs) for the online gaming industry, ultra vires regulations by states and a GST of 28% on amount “deposited with supplier” applicable for online gaming and casinos. Despite its rapid ascent in terms of game consumption, India’s online gaming segment constitutes a mere 1.1% of the global online gaming revenue. For the segment to truly thrive, a stable regulatory and legal framework is imperative. Uncertainties can impede the realization of its full potential and hinder rapid scalability.

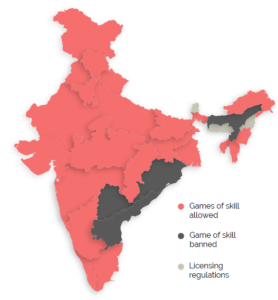

Responding to the urgency, the Central government announced online gaming rules in April 2023 to establish an unambiguous and self-governance framework for regulating the skill-based gaming sub-segment. The segment faced many regulatory challenges prior to the online gaming rules due to lack of a uniform framework. One key challenge has been on the distinction between the highly contested “games of skill” and “games of chance”. A game where success depends on preponderance or substantial degree of skill is a “game of skill”, whereas, a game where success depends on preponderance or substantial degree of chance is called a “game of chance”. Multiple courts have now ruled that online games are a “game of skill”, as opposed to gambling which is a “game of chance”. A player’s success or defeat in most online games depends on their capability (cerebral, motor-skill, or analytical), while in gambling there is no correlation whatsoever.

Moreover, gaming users play against one another, paying a small fee to the online gaming operators (OGP). However in gambling, players play against the house, where structurally the operator is one of the players. However, some states have amended gambling laws to include games of skill and prohibit the same in their states. For instance, Tamil Nadu government attempted to ban Rummy and Poker. However, the ban was lifted by the Madras High Court in November 2023 stating that Rummy and Poker are games of skill.

The uncertainty in the regulatory framework and potential regressive regulation by different states stand to severely damage the industry, stifle innovation and investor confidence. In order to adopt a unified approach and in furtherance of its commitment to advancing online gaming as a catalyst for “Digital India” initiative as well as promote a safe, trusted and accountable online gaming ecosystem, the Centre, in December 2022, notified allocating matters relating to online gaming to the MeitY. On 6 April 2023, MeitY notified the online gaming rules to provide a responsible and accountable regulatory framework for the online gaming intermediaries.

The rules call for setting up self-regulatory bodies (SRBs) which will be empowered to declare an online real money game as permissible if it meets the following criteria: Government feels that the SRB mechanism will help in curbing the growing menace of offshore betting and gambling platforms by ensuring that non permissible games are banned completely, including their advertisements.

However, much to the chagrin of the gaming industry, the formation of SRBs is delayed because MeitY is in the process of seeking consensus from various ministries and addressing concerns around independence of regulatory bodies. There has also been a MeitY proposal to take direct control of the approval mechanism for games and companies hosting them.

Then there is the bigger issue of GST. Extensive deliberations within the GST council over the past 12-18 months have brought about changes in levy of GST on the online gaming segment. In August 2023, amendments were made to the GST laws to specify that actionable claims offered by Real Money Gaming (RMG) platforms would be taxed at 28% on full-face value of deposits. In RMG format, a player purchases credits with real money and then plays games in which they can win more credits or lose all their current ones. Till 1 October, 2023, the RMG companies followed a practice of paying 18% GST on platform fees, also known as Gross Gaming Revenue (GGR). From GST perspective, skill-based gaming was intended to be taxed under “Other Online Content” taxable at 18%. Online gaming continued to pay GST under this classification, same as under the service tax regime.

In 2022, a government panel of ministers (GoM) submitted its initial report to recommend GST at 28% on Contest Entry Amount (CEA) and after lengthy deliberations with different state representatives putting forth their initial views, the GST Council recommended to reassess the recommendations of the GoM. In 2023, during the 50th GST Council meeting, the GoM suggested to increase the tax rate on online gaming to 28%. However, due to a lack of consensus on the valuation base, the GoM suggested that the GST council

Accordingly, the RMG companies have been served with tax demand notices for prior years. So far, the department has issued tax demand notices to the tune of Rs 1-1.5 lakh crore to more than 40 RMG companies. India boasts of approximately 400 RMG start-ups. The implementation of the GST amendment will potentially impact the free cash flows of both major and minor players, thereby presenting challenges for their innovation initiatives. Industry stakeholders suggest that the GST amendment has impacted the unit economics of RMG companies bringing down profitability, and therefore affecting investor sentiment. Industry discussions with stakeholders reveal that unit economics of RMG firms have been hampered by the amendment, leading to a drop in earnings before interest, taxes, depreciation, and amortization (EBITDA) margins, which will result in a subsequent impact on valuations.

According to a report launched by Think Change forum, the illegal offshore betting market is estimated at Rs 820,000 crore (US$100 billion) and post the new GST regime is likely to grow to INR 1,801,540 crores at an alarming rate of 30% annually by 2026. The projected growth would lead to an annual tax loss amounting to Rs 672,205 crores by 2026. As per an interview of the CEO of one such online illegal offshore betting and gambling websites, these illegal platforms take at least US$12 billion annually. 28% GST in this amount annually is thus owed to the Indian government which is approximately US$2.5 billion.

As per a letter written to the Prime Minister’s Office in July 2023 by a consortium of 30 prominent domestic and international start-up investors, including Tiger Global, Peak XV Partner, and Steadview Capital, the amendment could potentially lead to a write-off of the Rs 20,000 crore capital invested in the sector, and is also expected to impact prospective investments, estimated to be at least INR32,000 crore in the next 3-4 years, thus impeding the growth of the gaming segment in India.

This is important, given the growing demand with gamers in India was expected to grow from 390 million in 2021 to 450 million in 2023. Globally India currently has a small market share of online gaming industry as compared to 23% and 25% share of the United State and China, respectively. However, with the 38% CAGR and 86% share of mobile gaming within domestic market, India can become a market leader in “mobile gaming”.

Amidst the current stalemate, the road ahead for industry stakeholders indicates efforts by online gaming platforms to reinvent their operating models. The companies are re-evaluating business strategies for sustained operations and growth in response to the GST amendments. Although some outcomes may include consolidation and slower growth, the segment’s resilience is poised to redefine opportunities despite the challenges.

Faced with an increased GST liability, industry sources and stakeholders anticipate industry consolidation, foreseeing smaller companies either winding up or undergoing acquisitions as they absorb the financial impact of GST while maintaining sufficient funds for marketing and customer acquisition initiatives.

On consolidation, India needs to find its response, point out industry stakeholders, with large foreign companies consolidating to create oligopolistic market. China’s Tencent is the biggest gaming company globally, and one of the biggest investors in leading foreign game studios, which have the most popular games in India currently.

Recently, Microsoft acquired Activision Blizzard for US$68.7 billion, Sony bought Bungie for US$3.6 billion. However, with incentives and strategic support for the sector, Indian companies will rise on the global stage and help in competing with Chinese and western companies, especially in the mobile gaming space.